Trupanion: Mispriced Coverage

An under-the-radar insurer quietly restoring its bite. By Benjamin Tan

If you have read my book Suit Yourself, you will know that Enneagram Type Fives gravitate toward the complex and the niche. We like businesses that require spreadsheets, transcripts, and patience. We prefer the intellectual challenge of finding obscure stocks, and that is exactly our pitfall—overthinking rather than keeping it simple, like buying the S&P 500 or investing in a large-cap stock. And we are often attracted to underdogs that the market has quietly dismissed because we have an intellectual urge to prove the market wrong.

Trupanion TRUP 0.00%↑ fits that mold exactly, so this may be my psychological trap. I am aware that my personal biases may be at play here, unconsciously nudging me to look for evidence to support my preconceived thesis about this puppy. I am therefore writing up this analysis to lean more into objectivity and further away from the unconscious pull that may be driving my conviction. I am also capping my exposure by staying within the capital limits of my Traditional IRA and not extending it to my larger trading account.

Taking my own medicine here.

Suit Yourself Is Now Out!

After years of reflection and writing, my debut book, Suit Yourself: A Portfolio Strategy for Every Personality Type, is finally out, published through Koehler Books. This side passion project brings together my professional and personal journey across psychology, personal finance, and the many ways our identities shape how we invest.

Trupanion: Capital Discipline Interrupted by Temporary Margin Collapse

Pet insurance is a niche sector, and insurance math is complicated. Trupanion management talks about targeting an internal rate of return of 30-40% on pet acquisitions, rather than adjusted EBITDA theatrics. That combination made Trupanion TRUP 0.00%↑ the kind of small, esoteric stock that rewarded deep work for a number of years at the height of its growth during COVID.

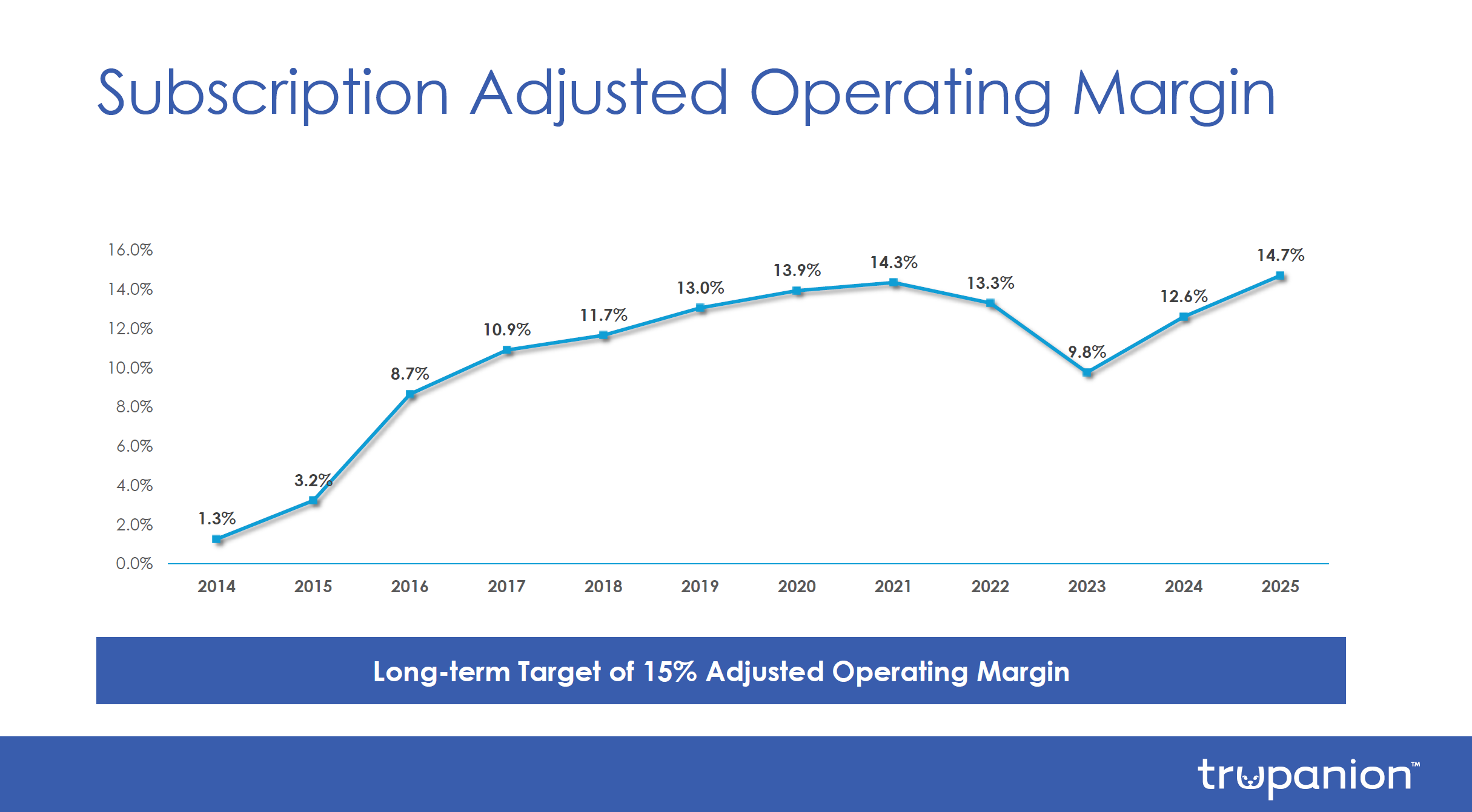

Strip away the noise in the last few years, and one can see that Trupanion’s business structure remains intact. Trupanion TRUP 0.00%↑ operates a cost-plus model: approximately 70% of subscription revenue is paid to veterinarians. The company targets a long-term, subscription-adjusted operating margin of about 15%. Excess capital is invested in pet acquisitions only if the projected internal rates of return are between 30% and 40%. This is not a traditional insurance approach; it aligns more with disciplined capital allocation within a subscription model. The margin drop in 2022–2023 was not a failure in strategy; it was due to pricing lag. Veterinary costs rose faster than premiums could be adjusted. Lifetime value temporarily declined. As a result, the market’s confidence faltered. However, pricing is now catching up. Margins are improving, and the financial guardrails remain in place.

The key question is not whether Trupanion TRUP 0.00%↑ can return to hypergrowth. It is whether normalized subscription margins of 15% are durable while the subscription business compounds in the mid-teens.

I believe they are.

Growth Has Slowed, But That is Not the Same as Broken

Between 2020 and 2022, when COVID prompted many to own pets, Trupanion TRUP 0.00%↑ was compounding revenue at 30-40%. Subscription pet adds were accelerating. Internal rates of return were consistently above target. The narrative was pristine.

Today, growth is mid-teens. That slowdown reflects three realities:

The pandemic pet boom pulled demand forward

Competition increased in digital distribution

Management intentionally moderated pet acquisitions while restoring margins

The veterinary channel remains the company’s structural advantage. Trupanion Express still differentiates at the point of care. Retention remains among the highest in the industry.

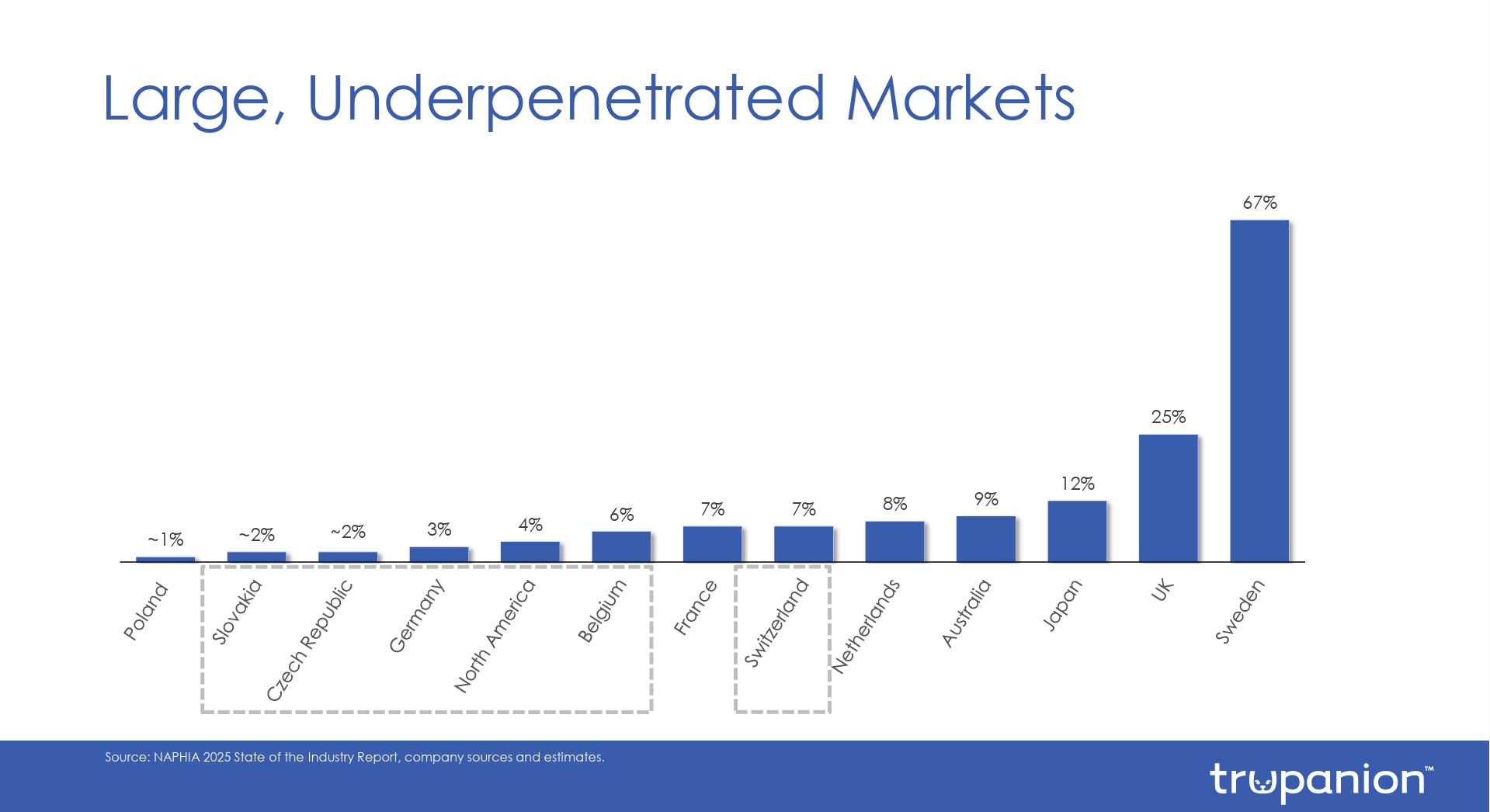

This is no longer a hypergrowth story but a disciplined specialty insurer operating in an underpenetrated category. Pet insurance penetration in North America remains low, and veterinary costs continue to rise. Those forces still support category expansion over time.

The key question is straightforward: can subscription revenue increase by 13% to 15% annually while preserving margin discipline and IRR targets? Keep in mind that Trupanion TRUP 0.00%↑ management is forecasting exactly that for FY 2026. If the answer to this question is yes, then the current valuation seems disconnected from its intrinsic value.

The Valuation Disconnect

At roughly $27 per share, Trupanion TRUP 0.00%↑ market capitalization is about $1.2b. Adjusting for cash and debt, its enterprise value is under $1b. That places the stock at less than 1x subscription revenue. For a business that has historically targeted 25% intrinsic value growth and deployed capital at 30% to 40% IRRs, that multiple implies structural impairment.

If subscription growth settles in the 8% to 10% range, the stock may simply be fairly valued. If growth stabilizes closer to 15% with normalized subscription margins of around 15%, the upside over a multi-year horizon becomes compelling.

This is not a bet on multiple expansion. It is a bet on durable underwriting discipline and mid-teens growth in a still underpenetrated category.

What Has Changed Since I First Bought It

I first bought Trupanion TRUP 0.00%↑ at $17 per share pre-COVID in my trading account. Back then, the appeal was explosive growth paired with strict capital guardrails. Today, the business is more mature. Growth is slower. Management replaced its CFO after a pricing misstep. Margin restoration took longer than expected. Yet the company is arguably more seasoned now. The balance sheet is solid. The playbook is clearer. Expectations are lower.

My Plan for Trupanion

My Traditional IRA position in Trupanion TRUP 0.00%↑ is currently small, under 2% of the account. I am fully allocated for Q1 under the deployment rules I set publicly. Barring a material deterioration in subscription growth or margin commentary in the upcoming earnings report, I intend to add in Q2 2026.

The bet is straightforward. I am underwriting normalized subscription margin durability and mid-teens growth. If that thesis holds, less than 1x EV/Sales for a disciplined, niche compounder looks attractive over a multi-year horizon.

This is not a comfort trade. It is a discipline trade. If margins hold and growth remains intact, intrinsic value should compound regardless of short-term sentiment. That is the bet I am willing to make.

My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. It examines how personality biases unconsciously influence investing behaviors. Learn more at my author page or order the book on Amazon. Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox