Upstart: An Automated Loan Division, Front to Back

Balance sheet exposure to auto-lending has overtaken the narrative – unfairly so

Traditional Bank Lending is Messy and Labor Intensive

I used to work on the arranger side of corporate loans. Over the course of a decade-plus, I was involved in more than 70 deals. Each deal was painful and labor intensive – from coordinating client onboarding and KYC clearance, to conducting due diligence and working with the back-office teams for post-funding maintenance. Almost all the steps were manual, down to the calculation of fees and interests — though Loan IQ was deployed, we would also use Excel to check and adjust. It took a village to get a loan from start to finish.

In addition to sheer man-hours, use of bank capital was rampant. Even though our business was designed to hold only a fraction (preferably none) of those high-risk loans on our balance sheet, we would often underwrite entire amounts for clients. Occasionally, we would get stuck with them, and some of the loans blew up. It was par for the course, no matter how much work was done to analyze credit risks, market appetite, and sell-down scenarios. Risk distribution to credit funds was complicated, overladen with paperwork, and often, imprecise. And if you thought institutional investors were much smarter than the rest of the human population, you would be wrong. Everyone in the ecosystem — from credit risk officers at the arranger side, to people working in debt funds — was just making educated guesses, but guesses nevertheless. Blind spots spared no one, and in hindsight, decisions had been made based on relationships, hubris, ego, and emotions.

Upstart Automation Engine — Front to Back Office!

When I came across Upstart (albeit it is in the personal loan space) I was drawn to their robust platform. In Q1 2022, 74% of their loans were fully automated, meaning those loans did not involve human intervention at all. Upstart had developed an AI-powered engine that could one day take over all the mind-numbing work from everyone at my former employers, from front office to back office! Even the distribution process was part of the Upstart platform, with institutional investors relying on its automated risk assessment in their loan purchase programs. How much more profitable, scalable, and precise my former divisions could have been, if manual labor and guesswork were removed from the business.

Capital-Lite, Fee-Based Business Model — Scalable and Profitable

Upstart makes more than 90% of its revenue from platform and referral fees, with additional sums providing services akin to back-office functions post funding. Its platform can be adopted by any lending bank, allowing one to expand without employing a mounting army of people to handle the messiness of a loan lifecycle. It is win-win for both Upstart and its partner banks. To me, Upstart’s value proposition looks compelling, having come from a loan origination and distribution background.

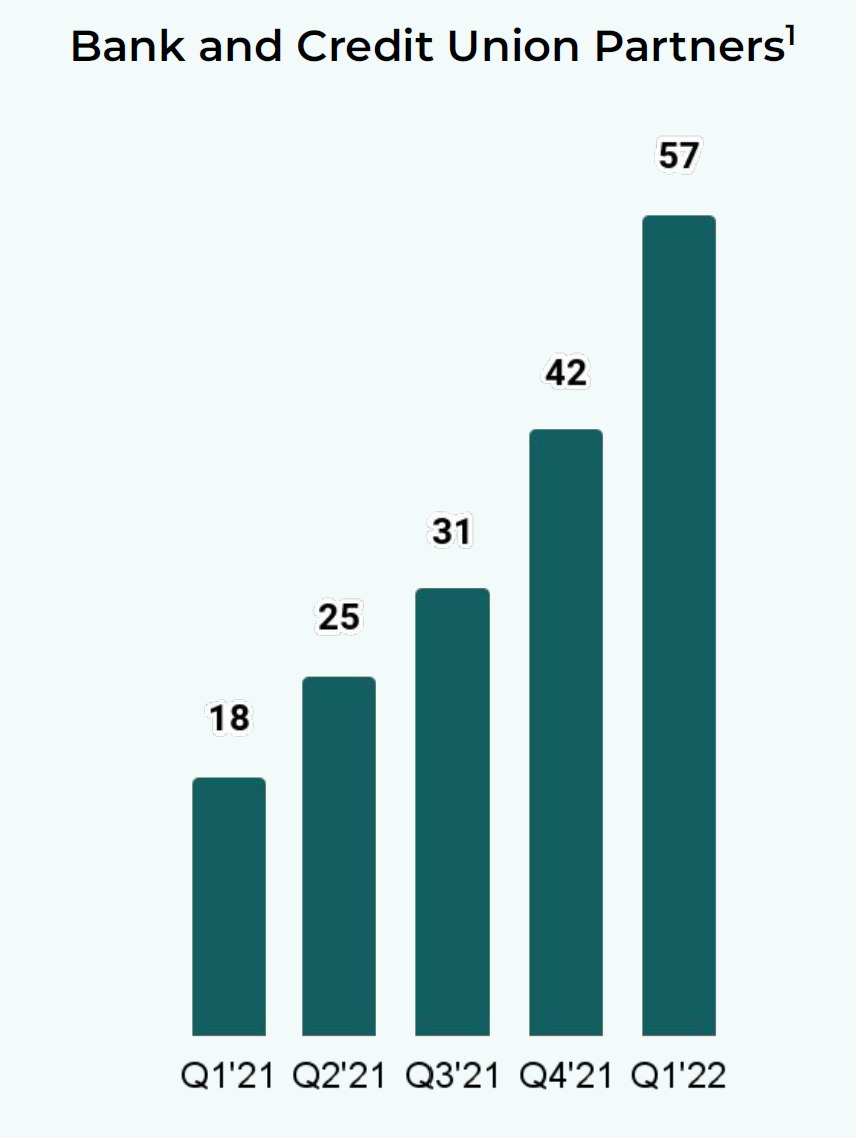

In Q1 2022, Upstart had 57 partner banks. This number is growing fast, validating the value of Upstart’s platform.

On average and on a per annum basis, each bank looks responsible for 50,000 loans with a combined value of $500 million. Upstart makes roughly $20-30 million of fees per annum from each bank, based on recent results. Apart from the initial 6 to 12-month implementation phase, platform running cost to Upstart at each partner bank looks marginal.

Consequently, contribution margin has been consistently above 40% since scaling up in mid-2020.

Upstart registered adjusted EBITDA margin of 27% in FY 2021, off a revenue base of $849 million. In other words, Upstart enjoys clear operating leverage, even with an average of only 40 banks in FY 2021. And Upstart has barely penetrated the personal loans market, with more promising lending products to come.

Changed Narrative Amid Market Turbulence

Recent narrative on Upstart shifted, after the company disclosed $600 million of auto loans on its balance sheet in Q1 2022. Management also admitted to overcommitment of its capital, amidst a volatile macro and interest rate environment. This has created plenty of anxiety for investors, and put in doubt the inherent nature of Upstart’s business model. Is it really a capital-lite platform, or a bank in disguise?

In fairness, that disclosure on auto-lending should not have come as a surprise. Back in Q4 2021, Upstart had already sunk $200 million (by my estimate) of its balance sheet to kickstart its auto-lending business. In fact, they guided to a total commitment of $1.5 billion for FY 2022. As was the case for personal loans, Upstart had to assume initial balance sheet risks (also called R&D loans by management) to prove out its AI-driven model before partner banks and institutional investors would participate in its ecosystem. For auto-lending – being secured and feeding off Upstart’s already proven track record in personal lending – that underwrite was more aggressive.

Going Forward — Some Unknowns but Thesis Remains Strong

How Upstart will pivot to manage its balance sheet exposure, and modify underwriting strategies for other lending products, is dependent on management execution. That is somewhat of an unknown at this point. It is also unclear to me how much the process of risk distribution to institutional investors is automated on the platform. From my read, the sell-down piece of Upstart’s ecosystem may be more manual than automated, though that can change. Given Upstart’s ambition to multiply in breadth and depth of lending products, balance sheet friction must be addressed by the automation platform. Mitigating the risks of getting stuck in the middle to material adverse effect is key to future platform expansion.

It is noted that Upstart is less than 10-years-old at this point, and even younger in its present form, since the company only shifted into the personal loan marketplace in 2014. The banks I worked at? Both over a century-old, and their underwriting mistakes much more severe. In the case of Upstart, it is an adolescent with growing pains. As it continues to scale across lending products and partner banks, snafus are inevitable. This is a risk that investors in fledging companies need to appreciate and accept. In any case, their current individual loan sizes are small — and auto-lending is collateralized — so diversification should at least mitigate the impact from macro factors.

Upstart’s core value proposition to partner banks and institutional debt investors remains unchanged. Given difficult (and expensive) hiring conditions, and an increasingly digital future, AI-driven automation is inevitable, especially for smaller credit participants. The addressable market is vast. I believe Upstart has plenty more potential than what the prevailing market narrative may suggest, as it continues to pursue product innovation, and automation up and down the lending value chain.

(Author is long $UPST)

Subscribe to Consume Your Own Tech Investing to receive a welcome email with the following:

Latest Top 10 conviction Consumer and Tech positions in my portfolio

3 book recommendations on investing, consumer and technology sectors

One article delivered into your inbox every Tuesday

Preview of upcoming articles

In addition, you will receive Subscriber-Only emails with updates to my portfolio convictions and latest recommendations on books to read.

Follow me on Twitter @ConsumeOwnTech