Zoominfo: Double Whammy

A tech company dependent on other tech companies for growth. By Benjamin Tan

Zoominfo (ZI 0.00%↑) Q2 2023 results were released last evening, and they disappointed on key metrics:

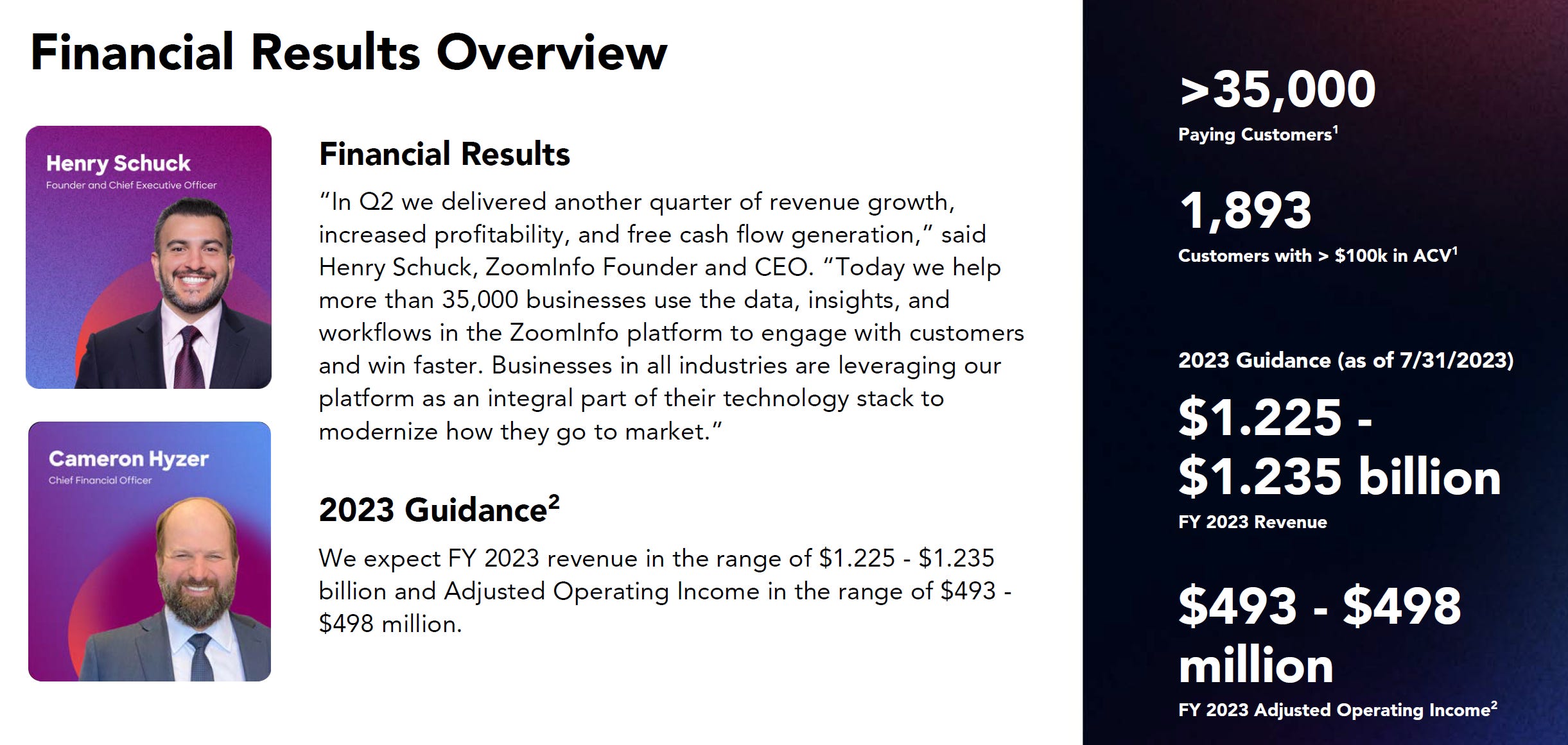

Quarterly revenue of $308.6mn fell short of management guidance ($310-312mn)

Full-year revenue outlook revised to $1.225—1.235bn (a reduction of $50mn at both ends)

Full-year non-GAAP adjusted operating income revised to $493—498mn (a reduction of ~$30mn at both ends)

Implied Q4 2023 revenue growth rate exiting at 4%, casting doubt on FY 2024 topline

Henry Schuck attributes the underperformance to weaker-than-expected contract renewals among software customers, who are hunkering down in survival mode, rather than targeting new businesses, for which Zoominfo’s core tools are built:

“…renewals really started to tick down much more than we expected…I think people are focusing more on their existing businesses than necessarily finding new customers…So while the kind of June impact had a modest impact to Q2, we have many more of those renewals coming up that were impact last year that we feel have some incremental risk at this point based on this first cohort of renewals coming through. And therefore, we want to make sure that we're taking a prudent view of the rest of the year and assume that those renewal trends worsen, which we think is the right way to set expectations for the second half.”

Seat Reduction, DownSell, and Linkedin

Zoominfo describes itself as “the go-to-market platform for businesses to find, acquire, and grow customers”.

With 35% of its customers in the software vertical, and the majority of them downsizing in the last 12-24 months since funding costs escalated, Zoominfo has seen worsening contract renewals from this segment. While gross retention has not deteriorated drastically, the number of seats renewed and downsells were far worse than expected:

“…we do expect gross retention to tick down a little. But more of the net retention in terms of our expectation is being impacted by fewer up-sells and more down sells…We are keeping those customers, but we are seeing the renewals being more challenging. And so yes, I think that is the real focus with respect to gross retention in 2023.”

To corroborate that the challenges facing Zoominfo are not unique to the company, management cited Linkedin’s latest quarterly revenue growth rate of 5%, which is also a dramatic drop from the 30% reported the year prior.

See below commentary from JP Morgan Research:

“However, we do believe that we underestimated the magnitude to which multiple lighting strikes to ZoomInfo’s core market could continue to weigh on the company’s near-term growth, factors that include ongoing macroeconomic sluggishness, sustained seat-compression across enterprises, disproportionate exposure to the software vertical and related layoffs, and the lingering effect of renewal pressure. We believe that these demand headwinds are not necessarily specific to ZoomInfo nor indicative of a meaningful competitive shift in this subsegment of the software landscape, as peers such as LinkedIn have also seen a material compression in growth, down to 7% in CC vs. closer to 30% a year prior (while the Marketing Solutions portion of LinkedIn was down y/y), and other public peers are seeing revenue contraction of as much as 24%.”

Earnings Call: Downbeat Tone

The Q2 2023 earnings call with CEO Henry Schuck and CFO Cameron Hyzer did not have the usual upbeat confidence. Despite calling out improving trends in April, the duo painted a different picture last evening, with Q3 and Q4 looking worse than Q2.

DBNR is expected to tumble to around 90% this year, despite continuing growth in the $1mn cohort and non-software verticals.

What Next?

My original thesis on Zoominfo is that the company helps customers optimize marketing budgets by improving targeting accuracy with its proprietary dataset and intelligence. Management maintains that its product suite remains relevant and superior compared to peers:

“Helping customers who have experienced the reduction in force on their go-to-market teams, redeploy ZoomInfo through a centralized data strategy, maintaining or increasing overall spend…As these companies and many across our customer base have realized, ZoomInfo's data is an infrastructural element to their CRM systems, sales campaigns, customer 360 initiatives, and their AI initiatives. With this, we see increased demand for our data and our data as a service business.”

Nevertheless, the key questions on my mind are:

How much are Zoominfo products worth to customers? Can customers do with lesser but cheaper products?

How much of the deterioration witnessed by Zoominfo is due to temporary macroeconomic headwinds, versus customers changing the way they purchase and value Zoominfo licenses?

Will competition force Zoominfo to drop prices permanently for better customer retention?

Is Zoominfo facing an existential crisis or will it surprise on the upside once hiring in the software vertical resumes?

It is somewhat unclear to me at this stage, and such is the risk of investing in smaller software companies that are outside the likes of Microsoft, Salesforce, and ServiceNow.

We do not know what we do not know.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

Latest Top 10 positions in my high conviction portfolio that combines value with growth stocks

Book recommendations on investing, consumer, and technology sectors

One article delivered to your inbox on Tuesdays

Preview of upcoming articles

Follow me on Twitter @ConsumeOwnTech and Commonstock @ConsumeOwnTech