Block: Addressing the Twin Elephants in the Room

Hypergrowth aside, Block is taking a lead among tech companies to confront GAAP profitability (Elephant #1) and stock-based compensation (Elephant #2). But is Afterpay Elephant #3? By Benjamin Tan

Block (SQ 0.00%↑) reported Q4 2022 earnings on February 23 and it was an unusual affair. Gross profits, excluding Afterpay (more on this below), grew a resilient 24%, with each of Cash App and Square surpassing Wall Street expectations. Instead of trumpeting this crucial outperformance immediately on the earnings call, co-founder Jack Dorsey began his opening remarks highlighting a brand new investment framework in which 2022 results fell short:

There are three principles guiding our investment framework:

Number one, ensure our investments are focused on customer retention and growth;

Number two, account for ongoing cost of the business, including stock-based compensation; and

Number three, utilize industry standard conventions that are simple to communicate and to understand.

Block, in each of our ecosystems, must show a believable path to gross profit retention of over 100% and Rule of 40 on adjusted operating income. This is an ambitious goal, especially at our scale, and one we aren't meeting today.

By addressing the twin issues of costs and stock-based compensation upfront on the investor call, Dorsey may be signaling a new era for Block. After all, with 2022 gross profits of almost $6bn - more than double that of competitor Shopify (SHOP 0.00%↑) - it may be overdue for GAAP profitability. Current markets have switched from “growth at all costs” to “show me the money” since interest rates started skyrocketing.

Under the new investment framework, Block’s adjusted operating income, taking into account the cost of issuing stock-based compensation, registered Q4 and full year 2022 losses of $32mn and $145mn, respectively. FY 2023 is guided to produce a similar level of adjusted operating loss as FY 2022.

Q4 2022 Earnings: Some Key Highlights

Profitability and losses aside, Q4 2022 earnings did assuage investors with continuing momentum at both Cash App and Square verticals. Below are some highlights from the earnings report:

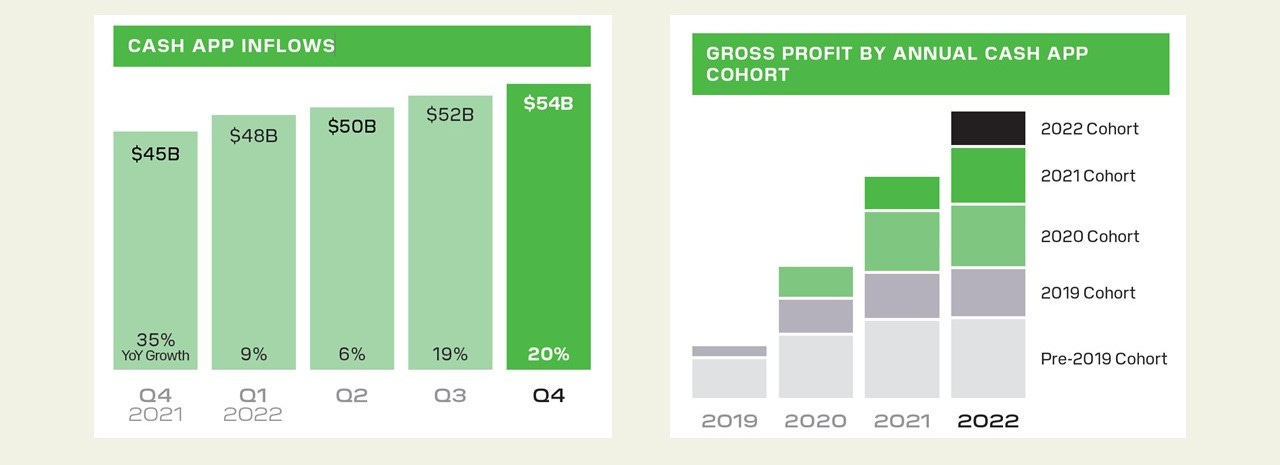

Cash App gross profit growth of 45% (excluding Afterpay) outpaced all estimates; strong cash inflows into user accounts also bode well for future funding costs to maintain a cost-efficient payment eco-system

Cash App Transacting Active grew by 16% to 51mn; more importantly, each cohort acquired in recent years demonstrated expanding usage and gross profit contributions

Excluding gross profit from PPP loan forgiveness and Afterpay, Square gross profit increased 17% - this is comparable to Shopify (best of breed in the category)

Square continued to be sticky with a mix of hardware and software adoption; DBNR (measured with gross profits) exceeded 100% and payback remained six quarters or less

Mid-market sellers (>$500k GPV) outpaced smaller merchants; this cohort represents the largest opportunity for Square

International growth is another S-curve for Block: Square GPV across international markets increased by 39%, beating domestic growth of 13%

Step-up in hiring over the course of 2022 amped up G&A and R&D costs; loan losses also ballooned due to Afterpay inclusion. Amortizations stemming from Afterpay added another $100mn+ in operating expenses. As a result, GAAP operating expense increased by more than 50% in FY 2022, taking GAAP EBIT down to negative $600mn+

Afterpay: Bought for $29bn and Paying More Later?

Afterpay was acquired by Block in January 2022 for $29bn in an all-stock transaction. It is a popular Buy-Now-Pay-Later (BNPL) service that represents the largest pivot that Block has ever made in its corporate history. It was also an expensive acquisition made at the height of the technology bull market and BNPL fever, with $12bn of resultant goodwill sitting on Block’s balance sheet.

Going into Q4 2022 earnings, I was expecting Block to take a write down on the goodwill, given higher interest rates, weaker consumer sentiment, and drastic drop in peer valuations, notably of Klarna and Affirm (AFRM 0.00%↑). It did not happen, but it remains a risk factor.

Much will depend on Block management as it continues to extract value from the lofty price paid. Execution risks are numerous, not to mention added balance sheet burden of providing consumer financing on a broader scale. Block is still integrating Afterpay into its existing Seller and Cash App business units, to “enable even the smallest of merchants to offer BNPL at checkout, give Afterpay consumers the ability to manage their installment payments directly in Cash App, and give Cash App customers the ability to discover merchants and BNPL offers directly within the app.”

For FY 2022, Afterpay contributed $588mn of gross profit but allowances for credit losses amounted to $197.6mn, in addition to overheads. Block maintains that loss rates - across Square Loans and BNPL consumer receivables - remained consistent within historical ranges. Afterpay, however, is a significant drag on Block's consolidated profitability:

With the Rule of 40, we are targeting the sum of our gross profit growth and adjusted operating income margins to be at or above 40% over the long term. This target applies to Block at the overall company level, as well as each of our ecosystems. By comparison, for 2022, Block's gross profit growth plus adjusted operating income margin was 33% or 23% excluding Afterpay.

While Afterpay may seem like an excessive purchase, the jury is still out there on this acquisition, whether it will reward Block shareholders in the long run, or make them pay more later in value destruction. In the near term, however, Block will need to do something more than just integration to accelerate its path towards the Rule of 40. In other words, Afterpay may be Elephant #3 under the new investment framework, but Dorsey largely ignored it on the investor call.

(Author is long Block)

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

Latest Top 10 positions in my high conviction portfolio that combines value with growth stocks

Book recommendations on investing, consumer and technology sectors

One article delivered into your inbox every Tuesday

Preview of upcoming articles

Follow me on Twitter @ConsumeOwnTech and Commonstock @ConsumeOwnTech